Effectively Casting Your Vision To Your Team as a Business Owner

February 18, 2021

How to De-Stress the Areas that Cause Business Owners Stress

March 4, 20217 Reasons Why Small Businesses Fail

I’ve often said that being an entrepreneur is one of the most rewarding jobs a person could ever have. However, any gains made as an entrepreneur come through hard work, sacrifice, and the ability to fail and get right back up again. Most business owners are okay with the early mornings and late nights. They even accept the fact that they’re going to miss out on a few of life’s moments and pleasures while they grow their business. But nobody wants to fail. In today’s post, I will discuss that uncomfortable subject as I give 7 reasons why small businesses fail.

Follow Along With The Financially Simple Experience!

TIME INDEX:

-

- 00:45 – 7 Reasons Why Small Businesses Fail

- 02:58 – Failure to Create a Business Plan

- 05:13 – Failure to Investigate the Market

- 07:21 – Financing Obstacles

- 08:33 – Poor Marketing Decisions

- 09:57 – Failure to Innovate

- 12:06 – Expanding too Quickly

- 13:11 – Poor Management

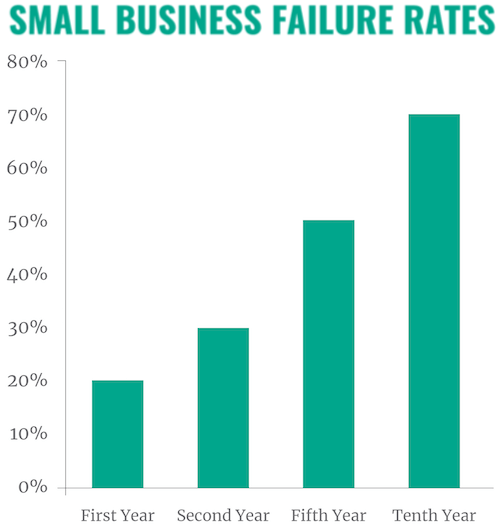

Small Business Failure by the Numbers

Small Business Failure by the Numbers

We all want to be good at what we do. I’ve never met anyone who made it their goal to fail. And yet, failure is often the precursor to success. There are very few entrepreneurs—if any—that were immediately successful business owners. In fact, data from the U.S. Bureau of Labor Statistics shows just how common failure is in the world of small business.

According to their findings, 20% of small businesses fail in their first year. That number increases to 30% in their second year, while 50% of small businesses fail after five years in business. Finally, 70% of small business owners fail in their 10th year in business. Depending on the type of business, these numbers can actually get worse.

For example, it is estimated that only around 30% of financial advisors survive after their third year. Realtors have an annual turnover rate of 88 percent. With numbers like that, it might seem like business ownership is a fool’s gamble. But if we understand why most businesses fail, we can put ourselves in a position to avoid making those mistakes. So, let’s take a look at some of the common reasons small businesses fail in the hopes of avoiding them.

#1. Failure to Create a Written Business Plan

It’s often been said that a failure to plan is a plan to fail. I truly believe this, and I often push clients to draft a fully-developed and written business plan. I don’t care if they’ve been in business for 20 or 30 years; if they don’t have a written business plan, then I’m pushing them to create one.

This isn’t a gesture of futility, either. There are many practical reasons for having a written business plan in place. Having a business plan can help you secure financing from lenders and investors. It can help you define and focus your business ideas and strategies. Not only will you concentrate on financial matters, but also on management issues, human resource planning, technology, and creating value for your customer.

Additionally, a business plan helps you identify potential pitfalls in your idea. You can also share the plan with experts and professionals who are in a position to give you invaluable advice. Likewise, business plans are a communication tool that you can use to share pertinent information about your business with stakeholders. Business plans may also convince people to work for you, secure credit from suppliers, and attract potential customers.

Having the business plan in writing means that you will always have it handy when you need it. However, writing out your business plan increases your odds of success on a subconscious level as well. A study by Dr. Gail Matthews of Dominican University in California found that people are 70% more likely to accomplish their goals when they put them in writing.

ADDITIONAL RESOURCES: How to Write A Great Business Plan

#2. Failure to Understand Your Market

Many small businesses fail because their owners didn’t take the time to investigate the market. I understand. As entrepreneurs, when we get a great idea, we want to make it a reality as quickly as possible. We have that mentality that we’ll charge hell with a water pistol. But when we’re dealing with something as significant as starting our own business, we need to slow down and conduct our due diligence.

Let’s say you’ve always wanted to own your own pizza shop. Sounds like heaven, right? You finally get the capital to open your shop, and you just set up in the first building you can afford. Unfortunately, this happens to be in an area of town that is heavily saturated with well-established pizza shops—if you know where this place is, please let me know because it sounds like heaven—that each has very loyal customers.

This is going to create a major barrier to entry. You’ve failed before you ever even began because you didn’t take the time to research the market. If you had, you would know that you needed to open in a different area and that pineapple on every pizza was a terrible gimmick!

A more realistic example involves a location in Knoxville, Tennessee. There is a restaurant space that I have seen turn over at least 8 times in my 17 years in Knoxville. It has a terrible entrance and egress and is just not situated in a good location for a restaurant. As a result, many business owners move in and end up shutting the doors within a year or two. If they had done a little research on the location, they might have been able to avoid such a fate.

#3. Trouble with Financing

A 2019 study by Guidant Financial found that 33% of business owners cited cash flow as their biggest challenge. There are several reasons for this, including poor cash flow management. If a business owner doesn’t understand how to use financing properly, they will go out of business.

It’s a simple concept, but many people struggle with it. If they’re constantly taking money out of business, lenders will not continue to offer to finance the business because they’re unsure how the business owner will pay them back. So, business owners struggling with financing is another one of the reasons their business fails.

#4. Marketing Mistakes

Marketing is an area that gives so many business owners headaches. I see business owners buy their marketing efforts from a salesperson all the time, and quite frankly, it’s one of my biggest pet peeves. If you own a business, you’re inevitably going to receive a phone call from your local monthly mailer advertising firm. They’re going to try to sell you advertising space in their publication.

Now, there’s nothing inherently wrong with these publications, and if it’s a part of your company’s marketing strategy, then great. But one of the reasons many small businesses fail is because they don’t have a marketing plan. Either they ignore marketing altogether, or they hemorrhage money into the wrong marketing campaigns. Today’s businesses must have an online presence, and they need to know exactly who they are trying to reach and how they can most effectively reach them.

#5. Failure to Innovate

It’s easy to become set in our ways. Especially when what we’ve done has been successful. However, there comes a time when business owners have to recognize the changing landscape and shift their companies to adapt to new ways of doing business. If there’s a positive to COVID-19, it showed us all just how important adaptability and innovation are to our businesses. The companies that were able to adapt to the new ways of doing business or that created innovative systems and products were the ones that really thrived in the midst of the pandemic. Those that were rigid and inflexible typically suffered.

One example of a company failing to change with the times is Blockbuster Inc. The movie rental giant was extremely successful throughout the 90s and saw its revenues decline drastically when Netflix introduced a new way to rent our favorite films. By the time Blockbuster finally adapted to the business model that Netflix introduced, Netflix had already moved on to the next big thing: a flat rate digital streaming service. In the end, Blockbuster fell victim to its own lack of innovation.

Wayne Gretzky, famously said, “I skate to where the puck is going, not where it has been.” There isn’t a better metaphor for innovation, in my opinion. We have to move to where the needs are going. A failure to innovate and keep up with the ever-changing needs and demands of the market can cripple small businesses and is one of the reasons that they fail.

#6. Expanding too Quickly

Any time we venture to expand our businesses, either physically, with additional locations or new markets, we open ourselves up to risk through new products and services. Without taking the same time and care during our expansion when first starting our business, we run the genuine risk of overextending our resources and harming our businesses.

Examples of growing too fast that can hurt your business:

- Losing track of finances.

- Cash flow mistakes.

- Overvaluing sales.

- Ineffective business operations.

- Hiring the wrong people.

- Not scaling customer service.

- Management mistakes.

- Scaling technology to business needs.

#7. Poor Management

Poor management is one of the biggest reasons why small businesses don’t survive. As a business owner, you likely got into business doing something that you’re passionate about. You’re highly skilled in your trade, but that doesn’t mean that you’re a skilled manager. In his book The E-Myth, Michael Gerber shares a story about Sarah, who liked to bake pies. Through managing her business, she found that she had lost her passion for baking pies.

Sarah hired a manager to take over the daily operating duties, and everything was going great until the manager was no longer there. She had placed all of her faith in this manager and didn’t know what to do without him. That’s a real problem for business owners who are great at their trade but not operating and growing a business.

Poor management leads to so many problems. This includes lost revenues through waste, poor efficiencies or quality control, inventory problems, unhappy customers, and low morale amongst your team. Poor management is a killer of small businesses, folks.

Wrapping Up…

Friends, there are risks involved in owning your own business. You know that. But taking lessons from where others have failed can give us an advantage. By learning from the mistakes of others (and from our own) can lead to success. We don’t have to suffer every failure on our own to receive its lessons. If you have concerns with any of these or other areas of your business, reach out to us. We help clients with problems like these daily. Reach out to us. Financially Simple’s team has helped hundreds of business owners work through these problems and drive toward achieving their long-term vision.