Would You Invest Your Money the Way You Are Going to Invest Mine?

October 6, 2017

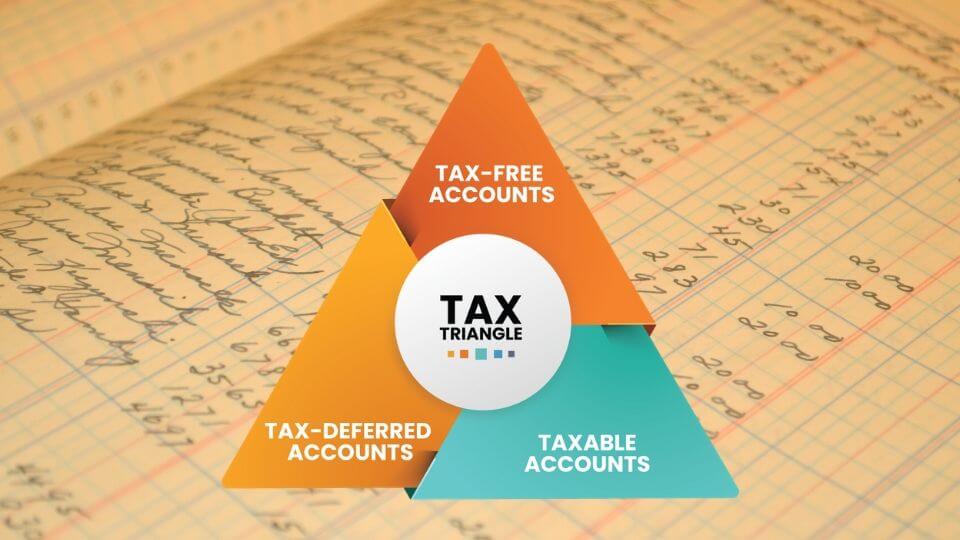

What is a Tax Triangle and Why Does it Matter

October 20, 2017Learning Asset Allocation at Age 60 – Advice to the Business Owner

When I first meet with a client concerning investment planning, I like to discuss asset allocation and how to utilize it for retirement. Granted I work with people of all ages, yet far too often I’m having the same conversation no matter the age. With more than half of all small businesses owned by Baby Boomers, I have more and more clients walking into my office looking to sell their companies and begin retirement. The problem is most business owners have 80% of their net worth tied up in their business. This means I’m having the exact same conversation with these owners that I’m having with my 20 somethings that are just starting out.

I have a particular client that decided to sell his business last year. We’ve spent the past 24 months working on the ins and outs of that transaction. The sale recently took place, and he ended up amassing a nice seven-figure amount even after taxes. What’s interesting about this individual is that he is in his mid-60s and just now trying to figure out how to fund his retirement.

Don’t get me wrong, that amount is plenty if utilized the right way. However, this person is accustomed to living on several hundred thousand dollars each year. If he continues that lifestyle without investing properly, he will be broke in a few years. Since he’s only in his mid-60s, his life expectancy could span another 30 years!

Obviously, this guy was great at what he did. He poured all his time and energy into a growing, thriving business. However, for the first time ever, he’s doing something he has never had to do—let someone else be in charge. As a CEPA and a CERTIFIED FINANCIAL PLANNER™ professional in Knoxville, TN, this individual sought me out for a few reasons. He wanted someone to walk him through the process of selling the business and making the income last a lifetime—at least his lifetime, if not longer. He was looking for a firm with someone close to his age—who could understand where he was in life—and someone younger than him, yet not a novice—so they would be around to help him in the management of his finances for the rest of his life.

Since his entire net worth was in his business, he’s never really dealt with investments such as stocks, bonds, and things of that nature. Utilizing his money for investment real estate didn’t interest him. He simply didn’t want to deal with someone else’s headache. His hope is to just retire and enjoy the retired life. Going places he’s never been. Seeing things he’s never had the chance to because he spent so much time working. He knows enough about finances to understand placing his money in a CD at the bank and only returning a measly 1% or so in interest rates won’t give him the lasting effect he is looking for. So he’s left working with a planner to help direct him on the things that he has no clue about.

This business owner is now telling me, “I wish I had learned this years ago. I wish I had someone telling me NOT to wrap everything up in my business this whole time.”

The truth is, he’d actually be even wealthier had he done it differently.

With the hope of taking time to travel and see the world in retirement, he’s got a great start with what he netted from selling his business. However, he’s also vetting the same issues that a 20-year-old business owner would be—making an income that will go the distance. That’s why I stress how vital asset allocation is to my young entrepreneurs.

This is a conversation that I have with 20 somethings beginning their career and planning for their future. Yet, I have to educate more and more, older business owners on these same principles. I’m spending a greater amount of time explaining how the markets work to them.

Undeniably the emotions that a 20-year-old and a 60-year-old will deal with in this situation are entirely different, especially when it comes to market volatility. One is just starting out and planning to attack retirement; the other is finishing up and trying to figure out how to keep retirement from attacking them. There’s no question that the financial behavior of the two age groups needs to be drastically different in order to reach their goals.

For example, if a 20 something invests $30,000, and the markets drop 20% it’s not that big of a deal. That’s not an insignificant number, but recovering from that at age 25 versus 65 is going to be different. If a 60-year-old has $10 million in the market, that same 20% drop now costs them 2 million dollars. The older person stands to lose a lot more at his age, not just monetarily but emotionally. That’s their whole life savings plummeting! Two million dollars to a 60-year-old who spent their entire life avoiding the market to build net worth is catastrophic! Helping them control their emotions in the face of market volatility is a challenge in and of itself.

We’re going to have tons of business owners selling their business in the next few years. Baby Boomers are going to be jumping out of the business world and into the markets for the first time. Now more than ever, it is so essential to understand asset allocation—especially if you have some time before you retire.

If you need help deciphering what to do in your own life, contact us. Our team is always here to help.

{kind=link}