Mortgage Debt: Pay It Off or Invest? Which Should I Do?

October 27, 2017

Tips for Effectively Communicating with Your Financial Advisor

October 31, 2017Millennials: The Wealthiest Generation Yet?

Millennials typically get a bad rap. Ask any baby boomer and you will likely hear how this generation is lazy with no vision. I actually had that very conversation recently with a client that is in his late 70s and very much a traditionalist. While some millennials may fit that bill, I’m finding quite the opposite to be true. The millennials I work with are actually very driven. They’re asking all the right questions to garner as much knowledge as they can about financial issues in a way their parents just never did.

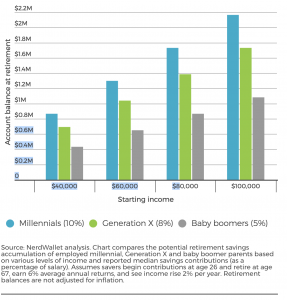

Whatever you think about Millennials, those aged 18-34, one thing is proving to be true. They save money at a greater rate than any other generation before—especially if the millennials are parents. A recent study conducted by Nerdwallet found that millennials with kids are saving 10% of the income for retirement. That is double the 5% the baby boomer generation stock away. Generation X is contributing on average just 8%. With that kind of laser focus, millennials will likely retire richer than their parents.

The study surveyed more than 2,000 adults. Just over 1,100 of those millennials were parents, while the rest had no children. Of those interviewed, 84% of those millennials with children were contributing to their retirement accounts. Additionally, 69% of those with no children were contributing as well. Millennials are making some unbelievably good financial decisions overall. They’re investing earlier and contribution more than their parents. Not only are they saving well, but they stand to inherit a good deal from their parents—making them possibly one of the wealthiest generations ever.

Let’s break down what retirement might look like for this generation. A 25-year old that just graduated college landed their first job and immediately set their sights on retirement making $40,000 a year decides to save 10% as Nerdwallet suggests. That comes out to $4000 a year they are socking away for retirement. Their monthly deposit is $333 a month. The plan is to work for the next 40 years and save save save save. No change made in the amount over that period of time. We invest aggressively. And we’ll assume an ROI of 8%. With all of these variables, at age 65 they are looking at a retirement account value of $1,170,255.65.

I would say $1.1 million is a pretty good retirement account. That’s not even taking into account that they will likely increase that amount as they near retirement. It is also possible they could return a higher rate. Couple that with the fact that most will inherit some amount of money from the baby boomer generation. Comparatively speaking, this so-called “lazy, unfocused” generation is set to accumulate tremendous wealth.

As great as all that sounds, it’s important to note, that millennials are also scared of the stock market. With that being the case, I say this, if you’re a millennial and you’re reading this post, don’t be afraid of the market. If you have 30, 40, or 50 years before retirement, then invest aggressively. I’m 38 years old, and I invest aggressively. I want to make as much as I can while I can.

Talk with your advisor to find your comfort level. However, with that much time ahead, being conservative now will hinder you not help. Let the market do with the market does. Be aggressive! Let the market work in your favor while you’re young. Throttle back when you’re older.

If you’re not a millennial, then take a page out of their playbook and start saving 10% of your income NOW! Now is the time to play catch-up. There’s a considerable difference mathematically speaking with between saving 8% and 10%. While making cuts and changes may be tough now, you won’t regret the extra money later.

{kind=link}