Why Your Lifetime Savings Rate Matters

January 19, 2021

How Much Should Business Owners Pay for a House?

January 26, 2021Stimulus: Should Business Owners Pay Off Debt or Invest?

Recently, the government approved the second round of economic stimulus checks for the American people. With the influx of cash, many business owners are asking how it would be best put to use. In today’s post, we will address how business owners can use the stimulus to their advantage, using principles that can be applied to any sudden windfall. Should business owners use the stimulus to pay off debt or invest?

Follow Along With The Financially Simple Experience!

TIME INDEX:

- 00:45 – Stimulus: Should a Business Owner Pay Off Debt or Invest

- 01:33 – It Depends

- 05:57 – The Decision Tree

- 09:52 – Other Debts

- 13:47 – Taxes

- 16:10 – Investing

- 17:22 – Summary

Every Circumstance is Unique

I am approaching this topic from the context of the recent economic stimulus that the government passed because it’s something that everyone can relate to. However, the content that I’m sharing could just as easily be applied to money received as a result of an inheritance, court ruling, or even the latest run of the PPP. Yes, I know business owners who are actually doing just fine at this point but still received PPP money because they qualified for it during one-quarter, last year.

Regardless of how you came into the money, the question remains. Should business owners use the money to pay off debt or invest? Even though there are several different ways that an individual may come into extra cash, the answer—like the question—remains the same. It depends. You see, I say this all the time on my show. Every circumstance is unique. This is why I make a point to remind everyone to take the information that I provide as an educational piece but to discuss their unique circumstance with a qualified financial advisor.

With that said, I hate debt. I would rather give myself a root canal than take on debt. However, there are times when taking on debt or not paying it off makes financial sense. On the other hand, there are situations where the opposite is true. In fact, allow me to illustrate.

Pay Off the House… When It Makes Sense!

I had a client that came into a bit of a windfall. He and his wife came to me asking what their best course of action was with this money. Typically, I believe that the home mortgage should be one of the last debts that you pay off. However, in this person’s situation, I suggested that they go ahead and pay down their home mortgage with the money they received.

In this particular situation, the client had four different types of loans. They had a home mortgage, an auto loan, student loans, and business loans. So, out of all of their debt, I asked them to pay their home mortgage first. You see, they didn’t have a regular home mortgage. Instead, they had what’s known as a jumbo loan at just over 5 percent. It’s a big beautiful home and they had a ton of equity in the home.

The student loan would be paid off through normal payments in about a year. Likewise, their business debt would be paid off in about six years. As I began reviewing the numbers with our team, we realized that by putting some money into the home mortgage, we could knock it renegotiate the terms to a conventional loan with a thirty-year fixed rate of about 2.7 percent.

We could have invested the money and we might have seen a 7 – 10% return but when we did the math, the client was better served to pay down the mortgage in this situation. So, how do we know when to pay off debt or invest?

Click to expand

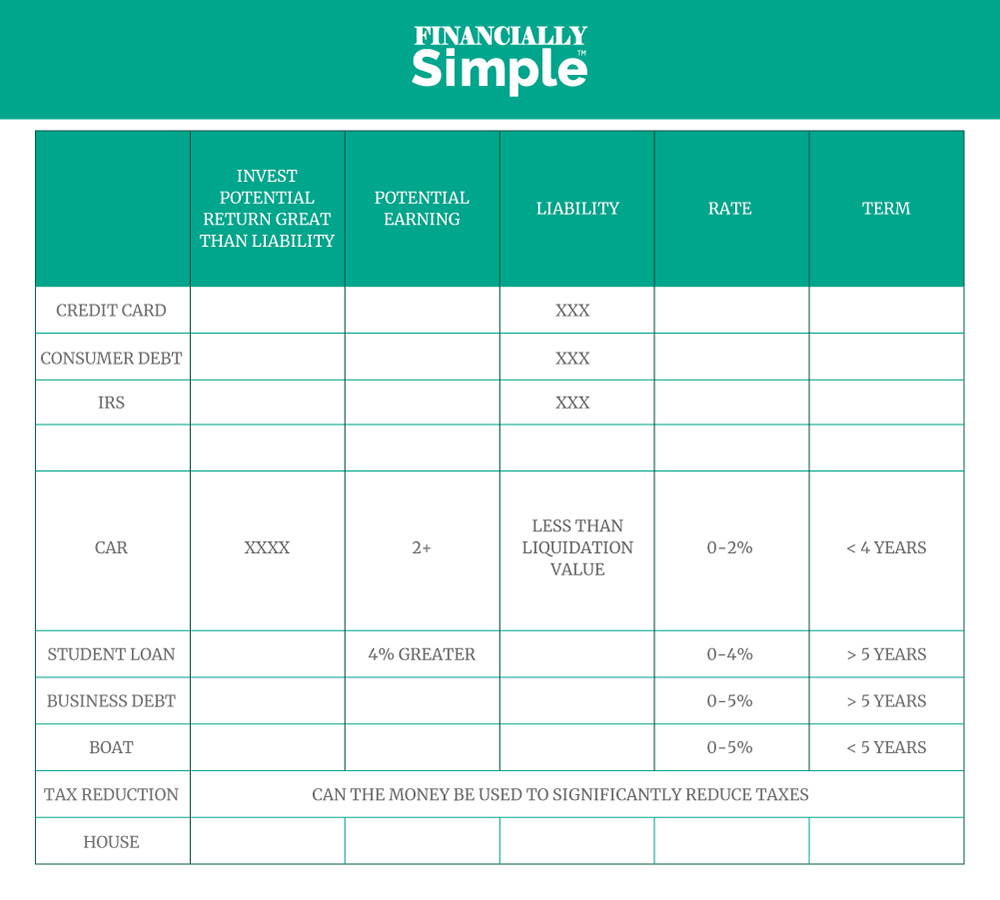

The Decision Tree

Before digging too deep into this section, I want to lay out my basic assumptions. These are the basic numbers that I use to figure up the long-term performance of my money given a specific decision. For starters, I assume a federal tax rate of 25 percent. Now, if you’re like me or many of my clients, you’re probably in a little higher tax bracket. But I go with a 25% rate at the very minimum.

Next, I look at the rate of return on my investments. For this, I typically figure at around 8 percent. I know that Dave Ramsey has said we can expect a 12% ROI but there are reasons that we can’t count on that. But for now, just know that I’m operating with an assumed 8% ROI. I also make the assumption that investment property is a tax play. Finally, when I’m dealing with cash, I assume that I’m going to have longer than a 10-year stint. With the assumptions out of the way, let’s look at my decision tree.

RELATED READING: Assuming an ROI for Wealth Gap Calculations

Let’s assume that I suddenly received $200,000 (although, this is an arbitrary number). The very first thing I’m going to look at is if I have any credit card debt. If the answer is yes, then the first move is to pay it off. Next, I look at my consumer debt. Let’s say I go to Bass Pro Shops and buy a brand new four-wheeler, using their financing options, that’s consumer debt, and I would pay that off next. The third non-negotiable is the IRS. If you owe anything to the IRS, pay them off! You do not want the IRS as a debt collector.

Other Debts

Other debts to consider when deciding to pay off debt or invest are unsecured debts and the IRS. You may not agree, and that’s okay. This is my decision tree. Feel free to make it your own, or even to make your own. Getting back on track, at this point, I go into a “yes or no” scenario. Let me give you an example…

Let’s assume I have a car loan that has a less than 2% interest rate. If I an auto loan at less than 2% interest, a debt that is less than the liquidation value of the vehicle, and a term less than four years, then I’m going to invest, or I’m going to move down the line. I have no credit card or consumer debt. I don’t owe the IRS. And my car loans aren’t upside down, have very low interest, and can be paid off in the next couple of years. Therefore, I’m moving down the ladder, still considering the possibility of investing.

Next, I look to see if I have student loans (I don’t, but many others do). If the answer is yes, is the interest rate below 4 percent? Does it have a term that is greater than five years? If it’s less than five years, just pay it off. However, if the interest rate is below 4% and the term is longer than five years, I might consider investing. From there, I’ll look at things like boats. Is the interest rate below 5%, and the term less than five years?

Taxes

I realize that many people would choose to pay off their house or their cars at a much faster rate. However, by deploying the cash differently, you could receive an instant bonus on your money. I have a friend that came into a windfall. I told them to place some of it into a 401k that had some profit-sharing built into it. Before they adjusted this windfall, they were in a 37% tax bracket. However, once they put the money into this 401k, they moved to an effective tax rate of around 27 percent.

Friends, that equates to an instant 10% bonus on their income, causing their investments to balloon as well. On top of that, they still get the return on the asset that they invested in. So, when I’m going through my decision tree and figuring out if I should pay off debt or invest, I see that I don’t really have much debt to hammer out. But now I’m asking myself if I can use this money for a tax play. If I’m able to get this type of instant bonus, I’m pausing here on my decision tree.

When and How to Invest

Now that I’ve walked you through my decision tree, you should have an idea of how to go about making the best decision for your unique circumstance. Once again, this isn’t advice. I’m only walking you through my own process for deciding if I should pay off debt or invest. Schedule a meeting with your financial advisor to go over your financial situation before making any major decisions. With that said, if you can say that you don’t have any credit card or consumer debts, you don’t owe the IRS, and your CFP® has already got you in a beneficial position for your future taxes, then I would choose to invest.

How you invest is entirely dependant on your individual financial situation. However, I always try to invest in a tax-sensitive manner. This means maxing out my health savings account (HSA), 401k, IRA, and Roth IRAs in order to grow my money while protecting as much of it as I possibly can from taxation. If you would like more information on this, please check out this video that I made a couple of years ago.

Friends, life is good. I know, it can get tough at times. But life is good. Deciding what to do with your stimulus can be frustrating, but with a quick assessment of your financial picture, we can make knowing if you should pay off debt or invest, at least, financially simple.

With all that is taking place in the financial and business world, are you certain that you’re in good hands? If you have questions about how to put the stimulus, PPP funds, or any financial windfall to work for you, schedule a meeting. The team of experts at Financially Simple has helped thousands like you.