Pass The Turkey, Comrade: What Thanksgiving Can Teach Us About Today’s Socialist Trend

November 26, 2020

Assuming An ROI for Your Wealth Gap Calculations

December 3, 2020How to Calculate The ROI of Investment Property

As we continue our deep dive into bridging the retirement wealth gap, I want to take a look at a subject that affects so many of us. There are so many people who deal with this type of asset that it is one of the largest types of asset holdings in the investment world. I am speaking, of course, of real estate. Up to now, we’ve tackled how to calculate our wealth gap, business ROI, and even taxes at the time of sale. But in today’s entry, we will focus on how to calculate the ROI of investment property.

Follow Along With The Financially Simple Bizcast!

TIME INDEX:

- 00:54 – How to Calculate the ROI of Your Investment Properties

- 02:23 – Investing in Real Estate

- 03:22 – Location, Location, Location

- 05:16 – Calculating ROI on Real Estate

- 09:26 – The Closing Costs

- 10:31 – Leveraging Mortgage Debt

- 14:43 – Summary

Real Estate Has Real Appeal

When I began researching this subject, I immediately took to the interwebs, as my dear old dad used to say. After doing a quick Google search for “how to invest in real estate,” I learned that this was a very popular topic. So popular, in fact, that it yielded 1.15 billion search results. Likewise, there are 114 million books on real estate investment and 287 million courses on the subject. I’d say that it’s pretty clear, real estate investing is one of the most popular investment vehicles in America.

Since the market decline leading up to 2013, people have been gravitating toward real estate investing. Many Americans saw their personal wealth deteriorate in the blink of an eye during that period and it shifted their way of thinking. The basic idea was that, with real estate, they could at least look at their property and see something tangible that they could sell. Couple that with the fact that it’s easier to borrow money for a large asset class than it is to make consistent savings moves.

The beauty of real estate investing is a simple fact that it allows us to leverage ourselves to reach our goals. But all of this prompted me to dig a little deeper. Since the focus of this article is how to calculate the ROI of investment property, I thought I should look at whether real estate investing is really the best way to go.

RELATED READING: Your Wealth Gap and Calculating Your Business’ ROI

Does Real Estate Really Offer the Greatest Return?

In a research paper by Kristin McKenna of Darrow Wealth Management, she showed some very interesting data on the performance of real estate by location. For example, New York City saw an average cumulative return on real estate investments of 158% between 1997 and 2019. On the other hand, real estate in Chicago only saw a return of 47%, which is drastically lower than the U.S. average of 126%. So, the old adage of “location, location, location” clearly has some merit. But, even with great returns such as these, is real estate the best investment vehicle?

| 1997 – 2019 | ||

| Region | Size Rank | Cumulative Return |

| United Stages | 0 | 126% |

| New York, NY | 1 | 158% |

| Chicago, IL | 3 | 47% |

| Washington, DC | 7 | 146% |

| Boston, MA | 10 | 185% |

| S&P 500 (TR) | N/A | 552% |

According to the S&P 500, it’s not. During the same span of time, the S&P saw an average cumulative return rate of 552%. Folks, that’s an amazing rate of return. Now, we know that past performance is not indicative of any future results and any assertion to the contrary is a federal offense. However, if we look at the historical context, we can see that real estate may not be as good of capital investment… right?

Well, in order to measure a return on investment, we need to see how much profit an asset class has provided. In order to calculate the ROI, we must divide the net gain by the total cost of investment.

How to Calculate the ROI of Investment Property

When you look at the equation above, you might think. “Justin, that’s so easy that my five-year-old could do it.” It’s true. The calculation is a very simple one. However, it becomes much more complicated when dealing with real estate. Here’s why. When calculating the ROI of investment property, we have to include things like maintenance expenses, whether or not we’re using debt and even vacancy rates.

In addition to these added variables, calculating the ROI of investment property is a little different when the property is purchased with cash instead of being financed. Let’s take a quick look at some of the differences.

ROI on Investment Properties for Cash Transactions

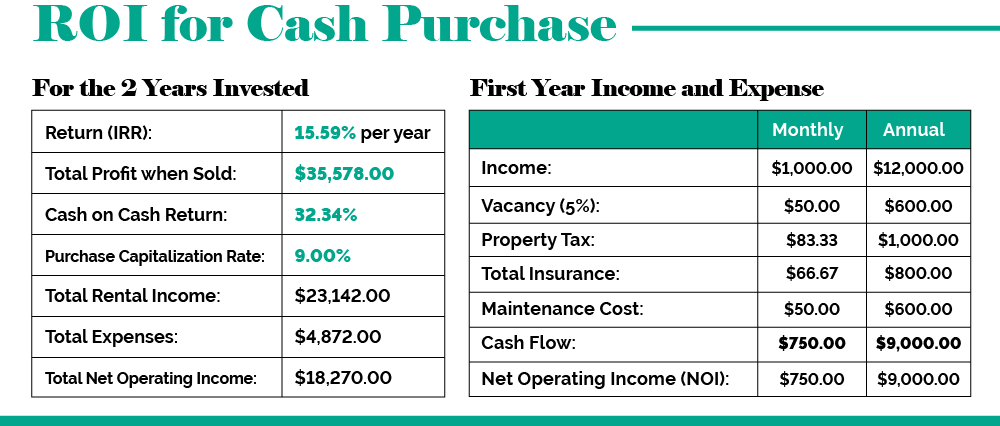

For simplicity’s sake, I’m going to provide an illustration using nice even numbers. Let’s say I went out and purchased a rental property for $100,000. Now, assuming closing and repair costs of $3,000 and $7,000, respectively, I’m all in for about $112,000 with a new property value of $120,000 after appreciation. At this point, I’m going to collect $1,000 per month in rent, and we’ll say that I’ve got a 5% vacancy rate.

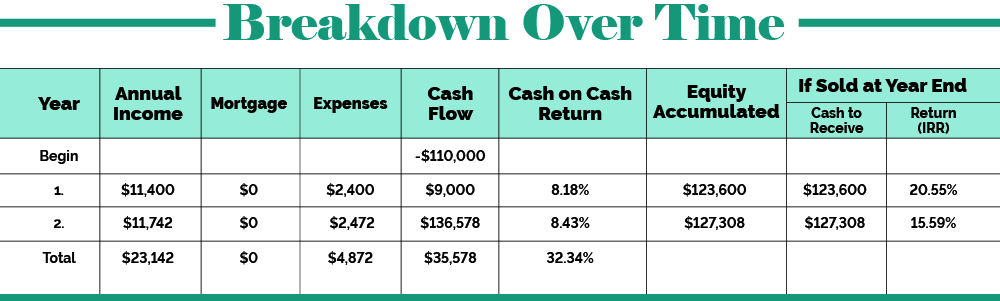

After one year, I’m still collecting my monthly rent and maintaining a 5% vacancy rate. But now, I have property taxes, lawn maintenance, and insurance fees that total $200 per month. And just for fun, let’s assume that the real estate value increased by 3%, as well. So, let’s look at how to calculate the ROI of investment property with these factors at play. Using our previous calculation, I would yield a 15.9% ROI by the end of year two. Not bad, right? If I were to sell the property at this point, I would make about $35,000 in profit.

After one year, I’m still collecting my monthly rent and maintaining a 5% vacancy rate. But now, I have property taxes, lawn maintenance, and insurance fees that total $200 per month. And just for fun, let’s assume that the real estate value increased by 3%, as well. So, let’s look at how to calculate the ROI of investment property with these factors at play. Using our previous calculation, I would yield a 15.9% ROI by the end of year two. Not bad, right? If I were to sell the property at this point, I would make about $35,000 in profit.

But let’s remove the 3% capital appreciation from the equation and only look at the dividend rate. How do we find that? The dividend rate is the amount of income we make, minus the expense of generating the income. In this case, we see a dividend rate of about 8.7%. If we include the 3% appreciation, we still have a cash-on-cash return of right at 8.5%.

But let’s remove the 3% capital appreciation from the equation and only look at the dividend rate. How do we find that? The dividend rate is the amount of income we make, minus the expense of generating the income. In this case, we see a dividend rate of about 8.7%. If we include the 3% appreciation, we still have a cash-on-cash return of right at 8.5%.

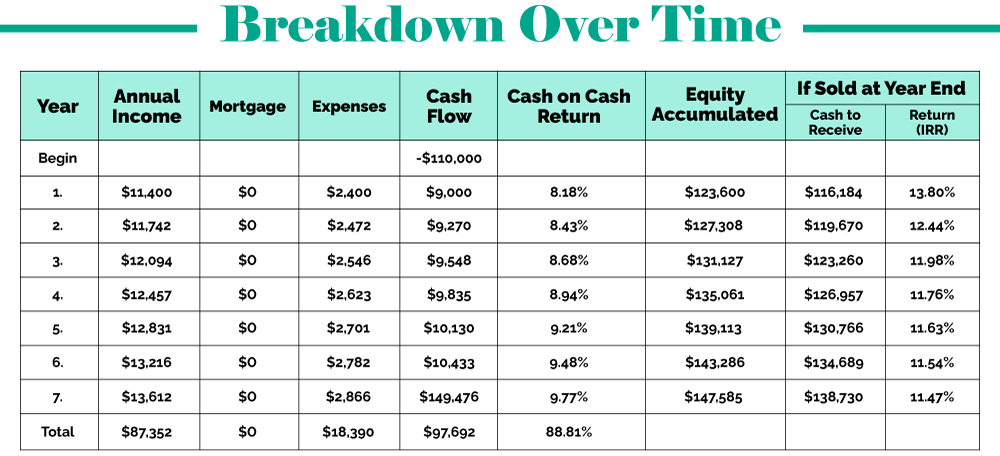

However, many investors miscalculate their ROI because they forget about the closing cost when it’s time to sell their property. The average length of homeownership in the United States is seven years. Using this average and the same numbers as before, we will assume that I am selling my property. After the 3% annual appreciation, I will sell my home for around $147,585 and receive $138,730 after closing costs.

RELATED CONTENT: Real Estate Investing – An In-depth Guide

ROI on Investment Properties for Financed Transactions

How to calculate the ROI of your investment property becomes a little more complicated when you purchase the property with debt. We’ll use the same numbers as before, for this example, but we’ll assume a $20,000 down payment on a mortgage with 4.5% interest. Because we are financing the property, the closing costs are a little bit higher at $4,000.

Anytime we deal with a mortgage, we also have ongoing costs that are associated with it. Again, we are going to keep the terms simple for this example. So, we’re going to assume a 30-year loan with a fixed interest rate of 4%. On the $80,000 that we borrowed, the monthly principal and interest payment would be $381.93. Just like before, we will add $200 for lawn maintenance, taxes, and insurance, bringing the monthly total expenses to $581.93. When we subtract the total monthly expenses from the $1,000 we receive for rent, we are left with a total monthly income of $418.07.

Therefore, after one year, we would have earned a total rental income of $12,000. This means that we have an annual return of $5,016.84 ($418.07 x 12 months). Now, in order to calculate the property’s ROI, we’re going to divide the annual return by our original out-of-pocket expenses (the downpayment of $20,000, closing costs, and remodeling for $9,000).

Once again, we’ll carry this example all the way to its eventual sale. After seven years, we have the same 3% annual appreciation. Therefore, when we sell the property, we are walking away with nearly $70,000. Folks, that’s a 235.55% cash-on-cash return. The less money we spend on the property, the greater our return. That’s why we typically fare better when purchasing real estate with debt. That’s how we make money on real estate investments. By purchasing with debt, we took an 11.47% ROI and turned it into a 23.79% return, friends!

Wrapping Up

Listen, there are so many things in this life that are beyond our control. Fortunately, our financial health isn’t one of them. With all that there is in this world, to cause us to be fearful, stressed out, and anxious, just remember that our businesses don’t need to be one of them, either. All it takes is a little knowledge and planning, and suddenly, the things that seemed scary to us, don’t seem like such a big deal.

Friends, life is hard. It is. But life is good. Calculating our ROIs can be frustrating but it doesn’t have to be. Take what you’ve learned, speak with your advisory team, and make bridging your retirement wealth gap at least financially simple!

If you have concerns about where you sit within your own wealth gap and ROI calculations, reach out to us. The team of experts at Financially Simple is here to help.