How to Calculate Your Income Savings Rate

January 12, 2021

Stimulus: Should Business Owners Pay Off Debt or Invest?

January 26, 2021Why Your Lifetime Savings Rate Matters

Do you ever think about how much money you’re putting into savings? What percentage of your lifetime income have you saved? The truth is, most of us don’t consider these things. But saving money for your future is one of the most important things you can do. That’s why I’ve chosen this topic for today’s post. Join me, as I explain why your lifetime savings rate matters!

Follow Along With The Financially Simple Experience!

TIME INDEX:

- 00:45 – How to Calculate Your Lifetime Savings Results and Why It Matters

- 01:07 – The Average Lifetime Income

- 05:10 – The Math

- 07:44 – How To Improve

- 10:33 – Summary

Social Security Findings

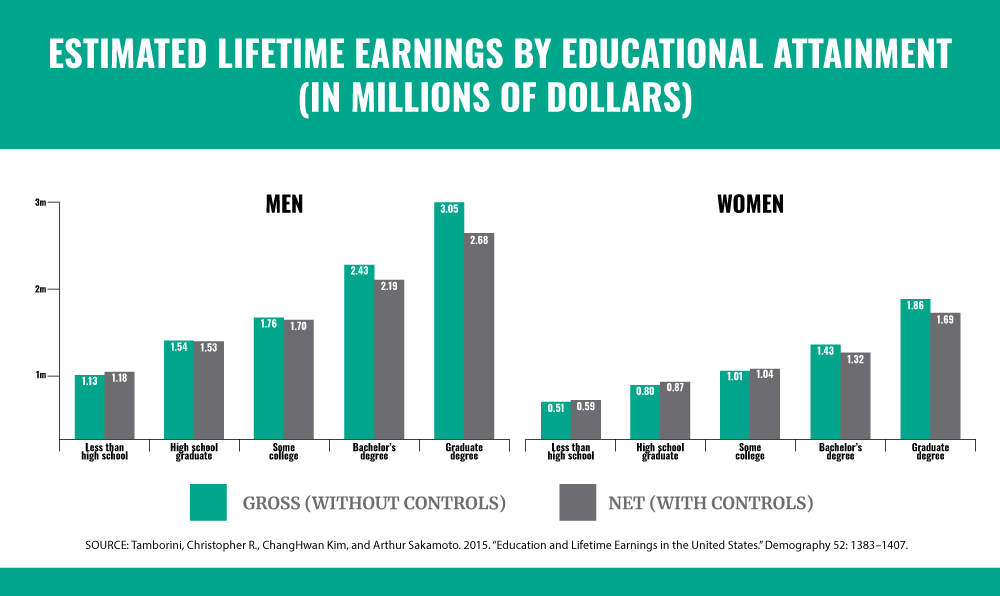

The Social Security Administration conducted a study back in 2015 that outlined the lifetime earnings of people with varying levels of education in the United States. I thought this was an interesting study because it provides us with a visual representation of the national average for lifetime incomes based on education levels. A male high school graduate can expect to earn somewhere around $1.5 million in their lifetime. On the other hand, if that same person achieved a graduate degree, they would earn around $3 million. Obviously, there are outliers and exceptions to the rule, but this is the average in the U.S.

SOURCE: Tamborini, Christopher R., ChangHwan Kim, and Arthur Sakamoto. 2015. “Education and Lifetime Earnings in the United States.” Demography 52: 1383–1407.

Let’s say that you’re on the upper end of this chart. If you did everything exactly as you should, you should have no less than $600,000 in income-producing assets by the time you retire. To be perfectly clear, $600,000 would be the minimum amount of assets at retirement assuming you didn’t invest your annual savings. Had you invested your annual savings, your retirement balance could be double, triple, or considerably more. But how did I get to $600,000? Well, going back to my last post, I said that you should be saving at least 20% of your gross annual income in income-producing assets. If you haven’t read it, go back and do so. If you have, how did you fair when calculating your income savings rate?

Even if you aren’t currently on pace with a 20% savings goal, don’t worry. It’s not too late. There are still things that you can do to improve.

It’s Not What You Make… It’s What You Keep!

Not long after recording the previous episode of the Financially Simple podcast, I met with a friend. As we were catching up, she asked what I’d been up to. I told her that I had just finished recording the episode and explained what it was about. This led to an interesting conversation. As I began to rattle off the data points and how to calculate your income savings rate, she made a statement that was concerning to me.

She said, “I’m paying down the principal debt of my business. So, I’m saving more than 20% because I’m building my net worth.” Technically, she was correct. She was improving her net worth, but only if the business was able to be sold. After she said this, I leaned back in my chair and asked, “Are you really playing roulette with your long-term future by using an asset that has a statistical likelihood of 15% to move from an illiquid asset to a liquid asset? Wouldn’t you rather use a more predictable asset as a buffer against the volatility of family-owned business?”

My reply left her speechless for a moment. I let her ponder that for just a moment and then explained the lifetime savings results to her. Friends, I always love having conversations like this because there is a moment where you can actually see the light bulb turn on in the mind of the business owner. She suddenly lit up and replied, “It doesn’t matter how much I make, it is how much I keep.” And that’s what this is all about. I’m not suggesting that you hoard it all and leave generosity by the wayside. But, as Matthew Kelly says in his book, The Dream Manager, “Those who don’t manage their money well are no better off than those who don’t have money to manage.”

Discovering Your Lifetime Income

In order to calculate your lifetime savings rate, you will need to discover your lifetime income. Now, there are a couple of different ways to do this. The first way is to look at your past tax returns. Yes, I have paper copies of every tax filing I’ve ever done and they are stored in chronological order. I thought it would be fun to, one day, be able to show them to my grandchildren and let them see where I began and where I finished.

However, if you’re not a nerd, like me, then you can request your Social Security earning information directly from the Social Security Administration. A third way is to request an income transcript from the IRS. But this last method is only available to people with fewer than ten years of reported income.

Regardless of how you find your lifetime income, you’re then going to divide that number by your current net worth. So, let’s assume that you’re worth $500K and that you have earned $2MM in your lifetime. That means that you have a lifetime savings rate of 25 percent. Friends, that is a sobering thought.

I remember the first time I made this calculation in my own life. At that point, Emily and I were worth roughly 120% of the total income we had received in our lifetime. My thoughts began to dwell on the future. If I’m going to earn $1MM, $5MM, $10MM, or whatever my lifetime income ends up being, how in the world am I going to build an account that’s large enough to replace my income. That’s the question I want you to ask yourself.

What You Can Do…

Now that you understand the gravity of your situation, you can make moves to improve it. First, you could increase your rate of return. Not too long ago, I had a friend that told me they were going to pay their home mortgage off. I told them not to do it and that I would make a video explaining why you don’t pay your house off. They listened and now have a greater net worth than if they had paid it off.

Another option is to increase your savings rate. If you’re currently saving 10%, why not increase that to 20, 30, 40, or even 50 percent? I know a person that gives away 90% of their income. When I first heard this, I thought it was impossible. But I’ve gone through their numbers and it’s true. What would your life look like—what would your giving look like—if you saved in such a way? I know that this isn’t feasible for everyone, but there are some of you who could actually do this.

Additionally, you can increase your lifetime savings rate through frugality and lifestyle choices. I’m not suggesting that you live on rice and beans while moving you and your family into a single-room efficiency apartment. But if you’re honest with yourself, there are probably several areas in your life that you could save some extra money for your future by cutting out or downgrading.

Wrapping Up

Friends, we only get so many years to prepare for the rest of our lives. Likewise, there’s only so much money that will pass through our fingers. Now’s the time to evaluate your savings strategies and measure them against your lifetime income. A little more effort now can make a huge difference later.

I know life is hard and we can’t always save what we should. But life is good, folks. Setting yourself up for the future can be frustrating but it doesn’t need to be. With the right calculations, determining your lifetime savings rate can, at least, be financially simple.

Are you dissatisfied with the results of your lifetime income and savings calculations? Whatever your results, the team at Financially Simple can help you improve them through carefully crafted savings and investment strategies. Schedule a meeting with us to determine how we can work toward the future you’ve always dreamed of.